Using this system, at the end of every month, or after your last paycheck for the month, do what I call “Paying Yourself.”

1. Total up your paychecks in the “Pay” section of your Tracking Budget. This is how much you have to work with for the next month.

2. Anything you paid for with cash – Handle this by referencing your ATM receipts and subtracting your ATM cash withdrawals from the Tracking Budget and on your checkbook register. (I recommend writing how much cash is intended for what on ATM receipts).

3. Sort your mountain of receipts into groups by the sections of your Budget (eg. Gas, Food, Me; and ATM separately), sum and subtract the totals of what you spent in each category from your Tracking Budget. See #3 below about credit card purchases.

4. Anything you paid for with your credit card – Subtract it from the respective section (for example, subtract the total of all your grocery receipts from Food), and add each total up to the “Credit Card” section. Then, I get a master total of all my credit card receipt piles and add that total up to the “Credit Card” section. When the cc bill arrives, I pay it out of the “Credit Card” section.

5. Get a new total for each section on your Tracking Budget. This way, you can see where you might have gone over/have a negative balance in that section. An example cause of this would be the shortfall from that leather jacket you bought, or that from spending more money on gas than you thought you would last month.

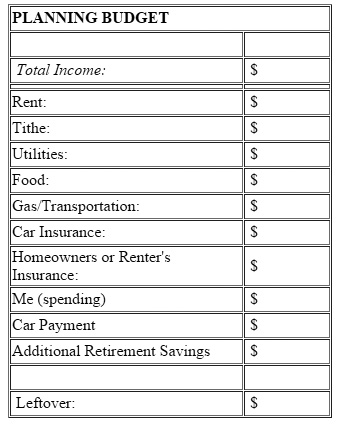

6. Now that you’ve dealt with everything you spent, reference your Planning Budget, and allot the amounts there by writing them into the respective sections of your Tracking Budget adding money to each. (Make sure to subtract all of the Pay section from itself. For example, $1800 – $1800=0 since you are distributing the full amount into sections of your budget.)

7. Ideally, you will have made more than the total of your regular expenses. Before you have a party about your discretionary (leftover) income, use the leftover cash to absolve any of the negatives we talked about in #5.

8. Anything you’ve got left after your negatives are taken care of is your final discretionary income. You can save that, spend it, or some combination thereof. Fun, fun, fun! Log how you’re using this money into your Tracking Budget. Time for totals…

9. Total 1 – You’ll get this from balancing your checkbook.

10. Total 2 – Get a full total by adding up the sections of your Tracking Budget.

11. Total 3 – Your Checking Account Statement total

12. Write total 1 and 2 on your checking account statement so you can see 1) Checkbook Register total and 2) Tracking Budget total vs. 3) Checking Account Statement total. Honestly, my 3 totals rarely equal, but as long as my Tracking Budget total is equal to or greater than my Checking Account Statement total, I’m happy since I spend based on my Tracking Budget.

13. If the total from your Tracking Budget is more than your checking statement shows, be careful as you spend for the forthcoming month. For some reason your budget shows more than your bank says you have. You may have subtracted something from one section and not added back to another. (For example, I’m guilty of subtracting something from say my Vacation Fund and forgetting to add it up into the Credit Card section of my budget.) Try to get these 2 totals to always equal since you’ll ideally want to spend based on your Tracking Budget not your current checkbook register total or online account balance.

WRAP UP – After “paying yourself,” put your pile of processed receipts in a different drawer, box, bag, etc., and at the end of that tax year along with your tax return paperwork, box them up, label, and store them. I like to group my ATM receipts together with any old checkbook registers and bank statements.

HOW OFTEN? – If you’re disciplined with your money, you can pay yourself and process receipts at the end of each month–this is by far the easiest way to do it. If not, you’ll need to do receipt subtractions more often to avoid overspending. For example, if you subtract what you’re spending on yourself in the “Me/Spending” section every week, you’ll easily see when you’re running out of pocket money for that month and can adjust. (Slow down spending on the fun stuff!)

FRESH BUDGET SHEET – When your Tracking Budget starts to get full, get a current total for each section, and start a fresh one, putting the date in the top corner. File the old one in with your processed receipts.

I know this process sounds very involved and may seem confusing, so check out this nifty to see the monthly “Paying Yourself” process in action!

Don’t miss a thing. Subscribe to receive updates by email.